Meanwhile, the household debt service ratio — measured as total obligated payments of principal and interest on credit market debt as a proportion of household disposable income — fell to 14.67 per cent from 14.81 per cent.

creditcardgenius.ca

^^^^^Some key statements in this article.

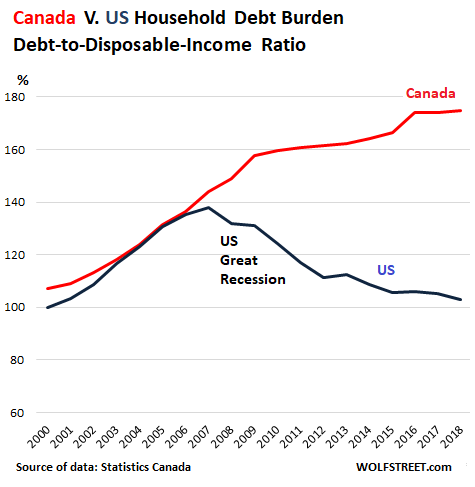

Should you care about the soaring Canadian debt ratio?

At this time, no. It has been on a steady rise for 30 years now. And, as you can see in the graph above, it has been relatively level for the last 5 years.

On an individual level, however, this isn’t the number you should be worrying about. The real number you need to consider is your

household debt service ratio. This ratio measures your ability to pay your debts.

Even if your full debt ratio number is 250%, it doesn’t mean you’re borrowing too much or living outside your means

Even if your full debt ratio number is 250%, it doesn’t mean you’re borrowing too much or living outside your means

Even if your full debt ratio number is 250%, it doesn’t mean you’re borrowing too much or living outside your means

Even if your full debt ratio number is 250%, it doesn’t mean you’re borrowing too much or living outside your means

^^^^^Repeated for Johnny.... must repeat information for him... he struggles with comprehension though

Mortgage debt and interest rates, not consumer debt, responsible for increasing debt ratio

With all that said, what has actually caused the increasing debt ratio?

Accounting for inflation, we’re paying more for mortgages, even with lower interest rates. But the increasing number is

caused by both the low interest rates and higher housing prices, with low interest rates making it easier to borrow large amounts of money.

The 177% number is calculated as the total amount of debt Canadians owe, divided by their disposable income for 1 year.

It’s an interesting number, but for most Canadians and lenders it’s

not a very useful number. It doesn’t truly reflect anyone’s capacity to actually pay their debts.

A better debt ratio to consider: household debt service ratio

A better debt ratio number is the household debt service ratio. This takes your gross income and compares it to what you’re actually paying on your debt.

It’s a better ratio that takes into account how much you’re making and how much you have to pay towards your debt.

Is there a magic threshold you want this number to be under? Generally, you’ll want to

keep your debt service ratio under 43% (which is what lenders usually use).

So far this year, the average debt service ratio in Canada has actually decreased – from 14.81% to 14.67%. Meaning, most Canadians are well within their means to pay what they owe.

^^^^^And Johnny wonders why I use what he calls finger puppets... because dealing with you is like dealing with kindergarten students. It's like I'm wiping your ass because you can't do it yourself(get reliable data). Now please give your friend Pierre Poilievre a call and see if he can baby sit you tonight!!!